How the Ukraine War Changed Europe: A Geopolitical and Economic Transformation

A deep analysis of Europe’s security, economy, society, and energy system after Russia’s invasion of Ukraine

Executive Summary

- The war in Ukraine accelerated Europe’s shift from a market-centered economic community into a strategic bloc that integrates security, energy, industrial policy, and social resilience.

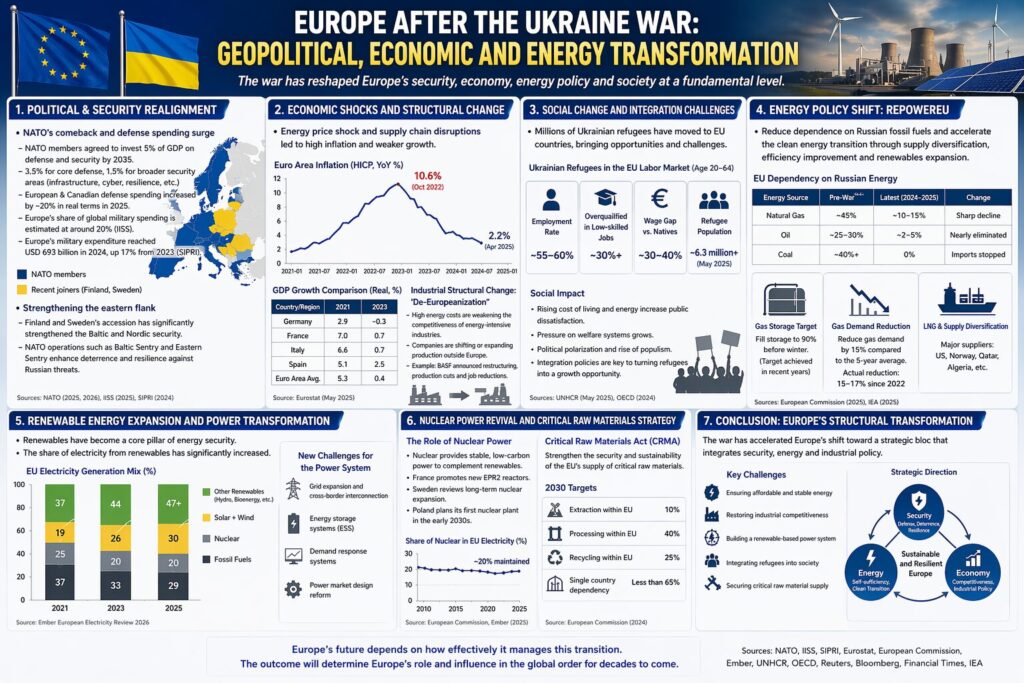

- European military expenditure rose to $693 billion in 2024, up 17% from the previous year, while NATO Allies agreed to invest 5% of GDP annually in defense and security-related spending by 2035.

- The EU cut its reliance on Russian gas from about 45% before the war to 12% in 2025, while Russian oil imports fell from 27% in early 2022 to 2% in 2025.

- In 2025, wind and solar reached 30.1% of EU electricity generation, surpassing total fossil-fuel power generation at 29.0% for the first time.

- Europe’s next challenge is to convert higher defense spending into real military capability while maintaining industrial competitiveness, energy affordability, and social cohesion.

- Introduction: The Ukraine War and Europe’s Zeitenwende

- The Reshaping of Europe’s Political and Security Order

- Economic Shock and Structural Reorganization

- Social Change and the Challenge of Integration

- The Energy Policy Turnaround

- The Rapid Expansion of Renewable Energy

- Nuclear Power and Critical Raw Materials

- Frequently Asked Questions

- Conclusion: Europe as a Strategic Bloc

Introduction: The Ukraine War and Europe’s Zeitenwende

Russia’s full-scale invasion of Ukraine on February 24, 2022, became one of the most consequential security shocks Europe has faced since the end of the Second World War. It was not simply a regional war. It disrupted the security architecture, energy supply structure, industrial competitiveness, and social integration model that Europe had built during the post-Cold War era.

Before the war, many European countries treated energy trade with Russia mainly as a matter of economic efficiency. Germany and several other major European economies relied on Russian pipeline gas as a stable and relatively cheap energy base for industry and households. Russia’s invasion and subsequent weaponization of energy exposed the fragility of that assumption.

Europe then changed direction rapidly. In security, NATO-centered collective defense regained central importance, and the accession of Finland and Sweden changed the strategic balance in Northern Europe and the Baltic Sea region. In the economy, surging energy prices and inflation pressured households and businesses, while energy-intensive industries faced higher production costs and stronger relocation pressure. In society, millions of Ukrainians sought protection across Europe, making refugee support and labor-market integration urgent policy challenges. In energy, REPowerEU accelerated the reduction of dependence on Russian fossil fuels while pushing renewable energy, nuclear power, and critical raw-material security higher on the policy agenda.

This report analyzes how the Ukraine war reshaped Europe’s political security order, economy, society, and energy system, and what this transformation means for Europe’s long-term strategic autonomy.

1. The Reshaping of Europe’s Political and Security Order: NATO’s Revival and European Rearmament

The Ukraine war fundamentally changed Europe’s security mindset. Before the war, many European states believed that economic interdependence with Russia could reduce the probability of large-scale conflict. Russia’s invasion showed that military threat remained a central reality of European security. As a result, Europe’s security discourse moved from “cooperation and economic interdependence” toward “deterrence, defense, and resilience.”

1.1 NATO Enlargement and the Structural Rise in Defense Spending

The clearest security change after the Ukraine war has been the rise in defense spending. According to SIPRI, total military expenditure in Europe reached $693 billion in 2024, a 17% increase from the previous year. This shows how the prolonged Russia-Ukraine war has pushed European countries to expand defense budgets at a much faster pace. Source: SIPRI, 2025

Germany’s shift has been especially symbolic. Chancellor Olaf Scholz declared a “Zeitenwende,” or historic turning point, shortly after the invasion, and Germany created a €100 billion special defense fund. This signaled a move away from Germany’s traditionally restrained postwar defense posture toward a more active role in European security.

The 2025 NATO Summit in The Hague institutionalized this shift. NATO Allies agreed to invest 5% of GDP annually in core defense requirements and defense- and security-related spending by 2035. This commitment consists of 3.5% of GDP for core defense expenditure and 1.5% for broader defense- and security-related investments, including infrastructure and resilience. Source: NATO Defence Expenditures and 5% Commitment

| Defense Indicator | Postwar Trend | 2024–2025 Status | 2035 Target |

|---|---|---|---|

| European military expenditure | Structural increase | $693 billion in 2024, up 17% year on year | Expected to keep rising |

| Previous NATO benchmark | 2% of GDP target | Many Allies reached or approached 2% | Superseded by higher benchmark |

| New NATO commitment | — | Agreed at the 2025 Hague Summit | 5% of GDP |

| Core defense spending | — | Expansion underway | 3.5% of GDP |

| Broader security spending | — | Infrastructure and resilience investment rising | 1.5% of GDP |

Table note: European military expenditure is based on SIPRI’s 2024 data. NATO’s 5% commitment reflects the 2025 Hague Summit agreement.

Some estimates suggest that Europe’s share of global defense spending moved toward the low-20% range by 2025, but such figures are estimates rather than finalized official statistics. Therefore, this report relies mainly on SIPRI’s confirmed 2024 data and NATO’s official 2025 spending commitment.

Finland and Sweden’s accession to NATO also transformed Europe’s security geography. Their membership significantly strengthened NATO’s strategic foundation in Northern Europe and the Baltic Sea region. However, given Russia’s presence in Kaliningrad, its Northern Fleet, and its hybrid-threat capabilities, it is more accurate to say that NATO’s strategic advantage and defense posture in the region were strengthened, rather than that the Baltic Sea became fully “NATO’s lake.”

1.2 Strengthening the Eastern Flank and Northern Security

NATO has reinforced its eastern defensive posture since the war began. Launched in January 2025, Baltic Sentry focuses on undersea infrastructure, maritime surveillance, and hybrid-threat response in the Baltic Sea. NATO described it as an effort to increase military presence in the region and strengthen Allies’ ability to protect critical infrastructure and respond to destabilizing activities. Source: NATO, Baltic Sentry

Eastern Sentry, launched in September 2025, is designed to reinforce air defense and deterrence along NATO’s eastern flank. NATO announced the initiative on September 12, 2025, and it followed incidents involving Russian drones entering Polish airspace. The move reflects NATO’s effort to strengthen air defense, surveillance, and deterrence procedures along the eastern frontier. Source: NATO, Eastern Sentry

Northern Europe and the Arctic have also become more important. In October 2025, NATO opened a new Combined Air Operations Centre in Bodø, Norway. CAOC Bodø strengthens air surveillance and command-and-control across Northern Europe, the Baltic Sea, the North Atlantic, and the Barents Sea. This shows how Russian northern military activity and Arctic strategic competition have become part of Europe’s broader security agenda. Source: NATO Allied Air Command, CAOC Bodø

1.3 Institutionalizing Support for Ukraine

European and NATO support for Ukraine has shifted from emergency assistance to longer-term, institutionalized support. The Prioritized Ukraine Requirements List, or PURL, emerged in 2025 as a mechanism through which NATO members finance the transfer of U.S.-made weapons and munitions to Ukraine. Reuters reported that PURL is structured so European countries provide funding while the United States transfers weapons, and that several packages had already been funded and equipment had begun moving. Source: Reuters, PURL mechanism

NATO and Ukraine are also working to analyze battlefield lessons and incorporate them into education, training, doctrine, and operational planning. JATEC reflects this trend. It helps NATO and Ukraine absorb lessons from drone warfare, artillery operations, electronic warfare, air defense, cyber threats, and hybrid operations observed on the Ukrainian battlefield. Source: NATO, Support for Ukraine and JATEC

2. Economic Shock and Structural Reorganization: Inflation, Industrial Competitiveness, and Relocation Pressure

The Ukraine war delivered two major economic shocks to Europe at the same time. The first was a surge in energy prices. The second was a shift in supply-chain and industrial cost structures. Europe’s dependence on Russian gas and oil made it vulnerable to sudden price increases and supply uncertainty, which in turn pressured both households and businesses.

2.1 Deteriorating Macroeconomic Indicators and the Policy Dilemma

In October 2022, euro-area inflation reached 10.6%, mainly driven by energy-price increases. Eurostat reported that euro-area annual inflation was 10.6% in October 2022, while EU-wide annual inflation was 11.5%. Source: Eurostat, October 2022 inflation

This high-inflation environment forced central banks into a difficult policy dilemma. They had to raise interest rates to control inflation expectations, while households and firms were simultaneously facing real-income losses and weaker demand caused by higher energy prices.

| Country or Region | GDP Growth in 2021 | GDP Growth in 2023 | Inflation Peak Around 2022 |

|---|---|---|---|

| Germany | 2.9% | -0.3% | About 11.6% |

| France | 7.0% | 0.7% | About 7.1% |

| Italy | 6.6% | 0.7% | About 12.6% |

| Spain | 5.1% | 2.5% | About 10.8% |

| Euro area | 5.3% | 0.4% | 10.6% |

Table note: The euro-area inflation peak of 10.6% is Eurostat’s official HICP figure for October 2022. National inflation peaks are summarized monthly peak figures around 2022 and are marked “about” because CPI and HICP definitions can differ by country.

These figures show how countries with strong industrial bases and high energy dependence, especially Germany, faced severe growth slowdowns after the energy shock. Germany recorded -0.3% GDP growth in 2023, revealing how vulnerable an energy-intensive industrial structure can be to geopolitical disruption.

2.2 Pressure on Energy-Intensive Industries

Europe’s chemical, steel, fertilizer, glass, and aluminum industries were directly affected by higher energy costs. Natural gas is not only a fuel but also a feedstock for chemical and fertilizer production. As a result, surging gas prices increased production costs and disrupted industrial supply chains.

Germany’s BASF moved to close some production lines at Ludwigshafen and cut around 2,600 jobs due to high energy costs and weaker cost competitiveness in Europe. This became a representative example of how strongly the energy-price shock affected Europe’s chemical industry. Source: AP, BASF job cuts and energy costs

The steel industry has also been affected by higher electricity prices and carbon costs. European steelmakers have argued that even with the expansion of renewable power, electricity-market pricing structures remain strongly influenced by gas prices. This shows that Europe must pursue energy transition and industrial competitiveness at the same time.

However, “deindustrialization” or “relocation out of Europe” should not be treated as a uniform process. Not every company is moving production abroad. Some are delaying investment, reducing output, closing selected facilities, or expanding new investment in the United States or Asia. Therefore, it is more accurate to say that energy-intensive industries face rising relocation pressure, rather than that large-scale relocation has already become inevitable.

2.3 The EU’s Industrial Policy Response

The EU has responded to the energy crisis, the U.S. Inflation Reduction Act, and China’s industrial-subsidy competition by expanding support for clean and strategic industries. The Clean Industrial Deal, the Critical Raw Materials Act, electricity-market reform, and more flexible state-aid rules all reflect Europe’s effort to preserve industrial competitiveness while advancing decarbonization and economic security.

Yet the challenges remain substantial. Europe faces high energy costs, complex permitting processes, uneven fiscal capacity among member states, and subsidy competition with the United States and China. In this sense, Europe’s postwar economic transformation is not merely a crisis response. It is a long-term redesign of industrial policy.

3. Social Change and the Challenge of Integration: Ukrainian Refugees and European Society

The Ukraine war triggered one of the largest forced displacement crises in Europe since the Second World War. Millions of Ukrainians moved to European countries, and the EU activated the Temporary Protection Directive to support their residence, education, healthcare, and labor-market access.

3.1 Labor-Market Integration of Ukrainian Refugees

According to UNHCR data, the employment rate of Ukrainian refugees aged 20 to 64 in Europe was about 57% by mid-2025. This indicates relatively rapid labor-market entry compared with previous refugee crises, but it was still around 22 percentage points below that of host-country nationals. UNHCR also found that many Ukrainian refugees were working below their skill level, showing a persistent problem of occupational downgrading. Source: UNHCR, Lives on Hold Report 2025

| Integration Indicator | Observed Status | Meaning |

|---|---|---|

| Employment rate, ages 20–64 | About 57% | Relatively rapid labor-market entry |

| Employment gap with host-country nationals | About 22 percentage points | Integration gap remains |

| Work below skill level | About 60% | Credential recognition and language barriers |

| Highly educated refugees in low-skilled work | Much higher than among locals | Human-capital underuse |

This creates both an opportunity and a challenge for Europe. Europe faces aging populations and labor shortages, while many Ukrainian refugees have higher education and professional experience. With language training, credential recognition, vocational support, and childcare assistance, they could help ease Europe’s shrinking labor supply.

Conversely, if refugees remain stuck in low-wage, low-skilled employment for long periods, Europe risks losing human capital and deepening social frustration. Refugee policy should therefore be treated not merely as welfare spending, but as part of labor-market, education, and regional-development policy.

3.2 Energy Costs and Political Polarization

Rising energy costs also intensified social tension. Low-income households spend a larger share of income on energy and food, so they are hit harder by inflation. After the war, higher electricity, heating, and food prices created conditions in which anti-establishment sentiment and far-right or populist politics could gain support in some countries.

This also affects energy-transition policy. Even if climate policy is necessary in the long run, citizens may resist carbon pricing, heating rules, internal-combustion vehicle restrictions, or building-efficiency standards if short-term costs fall heavily on households. Europe’s energy transition is therefore not only a technical issue. It is also a question of social acceptance.

4. The Energy Policy Turnaround: REPowerEU and the Strategy to Break Dependence on Russia

The Ukraine war forced Europe to rethink the meaning of energy security. Cheap energy is not always secure energy. Dependence on an authoritarian state can turn from an economic vulnerability into a security vulnerability.

4.1 The Sharp Decline in Dependence on Russian Energy

Through REPowerEU, the EU sharply reduced its dependence on Russian fossil fuels. According to the European Commission, the EU’s dependence on Russian gas fell from about 45% of overall imports before the war to 12% in 2025. Russian oil imports fell from 27% at the beginning of 2022 to 2% in 2025, while Russian coal imports were banned through sanctions. Source: European Commission, REPowerEU phase-out of Russian energy imports

| Energy Source | Prewar Baseline | 2025 Status | Change |

|---|---|---|---|

| Russian gas | About 45% in 2021 | About 12% | Sharp decline |

| Russian oil | About 27% in early 2022 | About 2% | Mostly reduced |

| Russian coal | High share in 2021 | Eliminated by sanctions | Effectively ended |

The gap left by Russian energy was filled by a wider range of suppliers, including the United States, Norway, Qatar, Algeria, and Azerbaijan. LNG became more important, and the United States emerged as one of the EU’s key LNG suppliers.

4.2 Gas Storage and Demand Reduction

The EU pursued not only supply diversification but also gas storage and demand reduction. The requirement to fill gas storage facilities before winter became a key energy-crisis response tool. However, storage management remains an ongoing policy challenge because LNG markets and geopolitical shocks can still affect Europe’s ability to reach storage targets. Reuters reported in April 2026 that the EU could face difficulty reaching its 90% gas-storage target before the following winter. Source: Reuters, EU gas storage 2026

Demand reduction was also significant. According to the European Commission, EU gas demand fell by about 17% between August 2022 and January 2025, equivalent to around 70 bcm annually. Extending the period to January 2026, the reduction reached about 19%, or roughly 80 bcm annually. Source: European Commission, REPowerEU 3 years

This reduction was not caused only by weaker economic activity. Lower heating demand, energy-efficiency measures, industrial process adjustments, fuel switching, and renewable energy expansion all contributed. However, lower industrial output also played a role, so the reduction should not be interpreted solely as an efficiency success.

5. The Rapid Expansion of Renewable Energy and Its Statistical Significance

The war elevated renewable energy from an environmental choice to a security necessity. To reduce dependence on Russian fossil fuels and lower energy-import costs, Europe accelerated the deployment of wind and solar power. Between 2021 and 2025, Europe’s electricity mix shifted rapidly away from fossil fuels and toward wind and solar.

5.1 Wind and Solar Surpass Fossil Fuels: Europe’s Energy Crossover

2023 marked the first year in which wind generation in Europe exceeded gas generation. Then, in 2025, wind and solar together reached 30.1% of EU electricity generation, surpassing the combined share of all fossil fuels, which stood at 29.0%. This was a symbolic “energy crossover.” Ember’s European Electricity Review 2026 also found that wind and solar accounted for 30.1% of EU electricity generation in 2025, compared with 29.0% from fossil fuels. Source: Ember, European Electricity Review 2026

| Electricity Source Share | 2021 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Total renewables | About 37.0% | About 44.0% | About 47.3% | About 47.7% |

| Wind | About 13.9% | About 17.5% | About 17.5% | About 16.9% |

| Solar | About 5.2% | About 9.0% | About 11.1% | About 13.2% |

| Total fossil fuels | About 37.0% | About 33.0% | About 29.2% | About 29.0% |

| Coal | About 15.0% | About 12.0% | About 9.8% | About 9.2% |

| Gas | About 19.0% | About 17.0% | About 15.6% | About 16.7% |

| Nuclear | About 26.0% | About 23.0% | About 23.4% | About 23.4% |

Table note: The 2025 figures for wind and solar at 30.1%, fossil fuels at 29.0%, nuclear at 23.4%, gas at 16.7%, and coal at 9.2% are consistent with Ember’s European Electricity Review 2026. The total renewables figure follows the original report’s classification, including hydropower, wind, solar, and bioenergy.

The 2025 figures show that renewable energy has become a core pillar of Europe’s electricity mix. Solar power, in particular, continued to grow quickly and became one of the central drivers of Europe’s power-system transition. Reuters also reported, citing Ember, that wind and solar overtook fossil-fuel power generation in the EU for the first time in 2025, while renewables supplied about 48% of total electricity. Source: Reuters, EU power mix 2025

However, this transition cannot be completed by capacity expansion alone. Wind and solar are variable sources of power, so Europe must also expand transmission grids, energy storage, demand response, cross-border interconnection, and grid-stabilization technologies. The next phase of Europe’s renewable-energy transition is therefore not only about generating more clean electricity. It is about building a power system capable of absorbing and balancing it reliably.

5.2 Leaders and Laggards in National Renewable-Energy Transitions

The pace of transition differs by country depending on natural resources, infrastructure, and political commitment. Denmark is widely seen as a European leader in wind- and solar-centered power transition. Austria and Sweden maintain high renewable electricity shares through combinations of hydropower, wind, and bioenergy.

Poland still has a high coal share and faces a more difficult transition. However, even Poland is reducing coal dependence compared with the past and is pursuing nuclear power and wind development to restructure its electricity system over the long term.

Germany continues to expand renewable power under the broader Energiewende framework, while the Netherlands has rapidly increased its solar generation and improved its renewable share.

6. Nuclear Power and Critical Raw Materials: Complementary Pillars of Energy Security

Alongside renewable-energy expansion, nuclear power has been re-evaluated in parts of Europe. When energy security, grid stability, and climate neutrality are considered together, some member states view nuclear power as a complementary low-carbon source.

6.1 The Reassessment of Nuclear Power

France continues to rely heavily on nuclear power and is pursuing new EPR2 reactors. Sweden has shifted toward a more nuclear-friendly policy stance, while Poland is planning to introduce its first nuclear power plant in the 2030s.

However, Europe as a whole has not reached a uniform pro-nuclear consensus. Germany has maintained its nuclear phase-out, and Austria remains strongly opposed to nuclear energy. It is therefore more accurate to say that nuclear power is being re-evaluated by some member states as a complementary tool for energy security and decarbonization, rather than that Europe as a whole is returning to nuclear power.

6.2 The Critical Raw Materials Act and Supply-Chain Security

The expansion of renewable energy and electric vehicles increases demand for lithium, nickel, cobalt, rare earths, copper, and other critical raw materials. Europe’s energy transition therefore reduces dependence on Russian fossil fuels while creating a new need to manage dependence on critical-mineral supply chains, many of which are linked to China or other concentrated suppliers.

The EU’s Critical Raw Materials Act is designed to address this vulnerability. By 2030, the EU aims to meet at least 10% of annual consumption through domestic extraction, 40% through domestic processing, and 25% through recycling, while limiting dependence on any single third country to no more than 65% for each strategic raw material. Source: European Commission, Critical Raw Materials Act

| Area | EU 2030 Target |

|---|---|

| Domestic extraction | At least 10% |

| Domestic processing | At least 40% |

| Domestic recycling | At least 25% |

| Dependence on a single third country | No more than 65% |

This policy is not the same as REPowerEU, but the two are connected through the broader logic of energy and industrial security. After reducing dependence on Russian energy, Europe must now manage vulnerabilities in critical raw-material supply chains, especially where processing and refining capacity is concentrated outside Europe.

Frequently Asked Questions

What was the biggest change in Europe after the Ukraine war?

The biggest change was Europe’s shift from an efficiency-centered economic community toward a strategic bloc that integrates security, energy, industrial policy, and social resilience.

How much did Europe reduce its dependence on Russian energy?

According to the European Commission, the EU reduced its dependence on Russian gas from about 45% before the war to 12% in 2025. Russian oil imports fell from 27% in early 2022 to 2% in 2025.

What was the key change in the EU electricity mix in 2025?

In 2025, wind and solar accounted for 30.1% of EU electricity generation, surpassing total fossil-fuel generation at 29.0% for the first time.

How is European rearmament progressing?

NATO Allies agreed to invest 5% of GDP annually in defense and security-related spending by 2035. Of this, 3.5% is intended for core defense expenditure and 1.5% for broader security, infrastructure, and resilience spending.

How are Ukrainian refugees affecting Europe’s economy?

Ukrainian refugees can help ease Europe’s labor shortages, but language barriers and credential-recognition problems have led many to work below their skill levels. Successful integration will require labor-market, education, and childcare policies.

7. Conclusion: Europe Is Transforming from an Economic Community into a Strategic Bloc

The Ukraine war imposed severe costs on Europe, but it also accelerated structural reforms that Europe had postponed for years. Before the war, Europe largely operated around economic efficiency and market integration. After the war, Europe has had to connect security, energy, industrial policy, and social integration into a single strategic framework.

In security, Europe is rearming around NATO. Defense spending is rising structurally, and the 2025 Hague Summit’s 5% commitment changed the benchmark for European defense policy. Finland and Sweden’s NATO accession, Baltic Sentry, Eastern Sentry, CAOC Bodø, PURL, and JATEC all show that Europe is moving toward a long-term deterrence posture.

Economically, Europe faced high inflation and weakened industrial competitiveness. Energy-intensive industries came under pressure from higher production costs and relocation risks, while the EU responded with clean-industrial and strategic-industrial policy. Yet high energy costs and subsidy competition with the United States and China remain major constraints on European industrial policy.

Socially, the integration of Ukrainian refugees remains a major task. Employment outcomes have improved relatively quickly, but occupational downgrading, language barriers, and credential-recognition problems persist. Successful integration could help Europe manage aging and labor shortages; failure could deepen social tension and political polarization.

In energy, Europe has made major progress in reducing dependence on Russian fossil fuels. Gas, oil, and coal dependence declined sharply, while renewable energy became a central pillar of the European electricity mix. Wind and solar surpassing fossil fuels in 2025 marked a symbolic turning point in Europe’s energy transition.

But the transition is not complete. Europe must solve four major challenges. First, it must convert higher defense spending into real military capability. Second, it must preserve industrial competitiveness despite high energy costs. Third, it must modernize grids and storage systems to support renewable-energy expansion. Fourth, it must manage critical raw-material supply chains and refugee integration as long-term strategic issues.

Ultimately, the Europe that is emerging after the Ukraine war is no longer just an economic community. It is becoming a strategic bloc that integrates security, energy, industry, and society. The success of this transformation will depend on whether Europe can move beyond Russian dependence, defend itself, secure energy affordably, preserve industrial competitiveness, and maintain social cohesion.

Key Sources

- SIPRI — European and global military expenditure in 2024

- NATO — Defence Expenditures and 5% Commitment

- Eurostat — Euro-area inflation at 10.6% in October 2022

- European Commission — REPowerEU and the phase-out of Russian energy imports

- Ember — European Electricity Review 2026

- Reuters — Wind and solar surpass fossil fuels in the EU power mix

- UNHCR — Ukrainian refugee labor-market integration

- European Commission — Critical Raw Materials Act

- Google Search Central — Helpful, reliable, people-first content

- Google Search Central — Article structured data